As the domestic property insurance sector looks ahead to 2026, one message is becoming increasingly clear: reinstatement cost inflation is not retreating. The construction environment that governs domestic repair and rebuild costs continues to face significant and persistent upward pressures.

For insurers, loss adjusters, repair networks, and valuation specialists, this is not just an economic observation—it is an operational and underwriting challenge that requires immediate recognition.

Construction Demand Is Rising, Not Stabilising

Recent ONS figures show continued growth across the construction sub-sectors most relevant to domestic property claims:

- Private housing repair and maintenance: +3.8%

- Infrastructure new work: +2.1%

These figures reflect sustained pressure on resources and supply chains—conditions that typically lead to higher costs for domestic repair works. Moreover, both Experian and the Construction Products Association (CPA) forecast further growth in 2026, with:

- RM&I output expected to grow 2.5%, and

- Overall construction output rising by 3.7%.

Higher demand in a capacity-constrained market almost always translates into elevated reinstatement costs.

Headline Inflation Is Rising

Most forecasts suggest UK inflation over the next 12 months will remain higher than the Bank of England's 2% target, with the most likely range sitting between 3% and 4%. The main drivers are expected to be higher energy prices, continued wage growth, stubborn services inflation and ongoing geopolitical uncertainty, particularly in the Middle East. While a return to the extreme inflation levels seen in 2022 is not currently the central expectation, economists believe prices will continue rising faster than many consumers anticipate, especially across utilities, insurance, food, construction materials and labour-intensive services. The overall outlook points to inflation easing only gradually, meaning interest rates and borrowing costs are also likely to remain higher for longer.

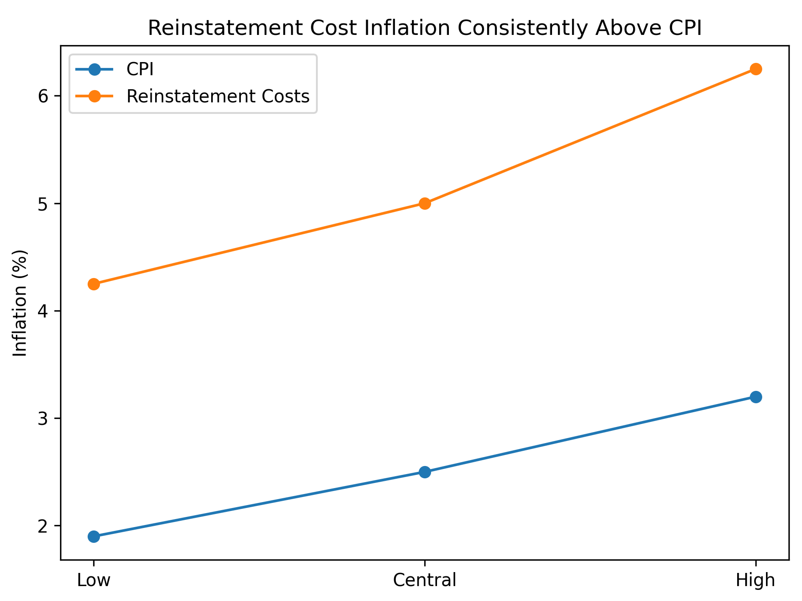

However, headline inflation is not a meaningful proxy for what is happening in construction, where labour shortages, material cost stickiness, and strong market demand continue to drive sector-specific inflation well above CPI.

This divergence is critical for insurers: policies indexed to CPI alone risk falling short of the actual rebuild and repair costs seen on the ground.

Labour: Structural Shortages Continue to Elevate Costs

Labour remains one of the largest drivers of domestic repair inflation. ONS data shows:

- Construction wage growth rose 3.5% year-on-year to July 2025.

Industry forecasters confirm this trend will continue:

- Arcadis expects 3–5% tender price inflation in 2026.

- BCIS projects labour costs rising 3% annually to 2030.

- BATJIC agreements include 3% wage increases for 2025/26.

Taken together, labour inflation for 2026 is expected to sit firmly in the 3–4% range.

Impact of the Iran Conflict

With many domestic claims reliant on skilled trades—roofers, plasterers, electricians, joiners—labour inflation translates directly into higher reinstatement costs. Growing conflict involving Iran and wider instability across the Middle East risks triggering another significant wave of construction cost inflation, driven by pressure on global energy markets, shipping routes, logistics costs and business confidence.

At the centre of the concern is the Strait of Hormuz, one of the world's most strategically important shipping routes, where any prolonged disruption could rapidly increase oil and gas prices, marine insurance and freight costs. This is particularly important for the construction sector because many core materials including steel, aluminium, cement, glass, insulation, plasterboard and asphalt are highly energy intensive to manufacture and heavily reliant on stable global supply chains. Early signs are already emerging, with suppliers beginning to report pricing pressure and shorter quotation validity periods.

Best Case Scenario – Managed Disruption

In the more optimistic scenario, the conflict stabilises relatively quickly, the Strait of Hormuz remains operational and global energy markets begin to settle over the coming months.

Under those conditions, UK construction inflation could remain relatively contained, likely averaging between 4% and 8% overall.

Best Case Cost Breakdown

| Material | Estimated Increase |

|---|---|

| Steel | 10%–15% |

| Cement & Concrete | 5%–10% |

| PVC & Plastics | 10%–20% |

| Glass | 5%–10% |

| Timber | 3%–8% |

| Logistics & Haulage | 5%–12% |

Worst Case Scenario – Prolonged Regional Instability

If disruption becomes prolonged, shipping instability increases and oil prices remain elevated for a sustained period, the industry could see construction inflation returning to levels closer to those experienced during the post-Ukraine supply shock.

Under that scenario, average construction cost increases could realistically move into the 12% to 20% range overall, with some material categories significantly exceeding that.

Worst Case Cost Breakdown

| Material | Estimated Increase |

|---|---|

| Steel | 20%–35% |

| Aluminium | 15%–30% |

| PVC & Plastics | 25%–40% |

| Asphalt / Bitumen | 30%+ |

| Cement & Concrete | 15%–20% |

| Glass | 15%–25% |

| Insulation | 15%–30% |

| Logistics & Shipping | 20%–50% |

The Bigger Risk – Uncertainty

But perhaps the bigger challenge would not simply be inflation itself—it would be uncertainty.

Volatile markets create defensive pricing behaviour. Contractors increase contingency allowances. Suppliers shorten quote periods. Procurement teams struggle to secure consistent pricing. Insurers face widening gaps between estimates, approvals and final account costs.

What This Means for Domestic Property Insurers

Despite improvements in the macroeconomic environment, home repair and rebuild costs remain elevated due to:

- Ongoing skilled trade shortages

- Stubbornly high materials costs

- Strong demand for RM&I activity

- Structural supply constraints

This means insurers who do not adjust their pricing, indemnity limits, and claims cost assumptions risk:

- Under-insurance (sum insureds lagging behind real-world costs)

- Increased claims severity

- Repair delays and customer dissatisfaction

- Higher indemnity spend

Final Thoughts

2026 will not be the year reinstatement costs return to historical norms. Instead, the domestic repair market will continue to experience inflation levels meaningfully above general CPI.

For the insurance industry, adapting now is essential. Appropriate uplift measures, accurate valuations, and clear communication with policyholders will be key to mitigating under-insurance, managing claims costs, and maintaining service resilience.

Failing to act means falling behind the real economy. Taking measured steps now keeps the industry aligned with the true cost of putting homes back to the condition they were in before the loss—and that commitment sits at the heart of what domestic property insurance is meant to deliver.